2023 Corporate income taxFinal settlement and settlement须知

In order to help Park tax friends understand the scope of application, declaration time, declaration method, declaration process and submission of information and other tax-related matters related to the 2023 corporate income tax settlement and settlement, the following matters related to the 2023 corporate income tax remittance are presented:

一、Scope of application of final settlement

Any taxpayer who engages in production or business operation (including trial production or trial operation) during the tax year, or terminates business activities in the middle of the tax year, regardless of whether it is during the tax reduction or exemption period, and regardless of profit or loss, shall be subject to the final settlement and payment of enterprise income tax in accordance with the relevant provisions of the Enterprise Income Tax Law and its implementing regulations。The branches of enterprises operating across regions shall also make annual tax returns in accordance with the provisions, calculate and apportion the tax payable and refunded according to the head office, and handle tax payment or refund on the spot。

(A) general enterprise remittance time

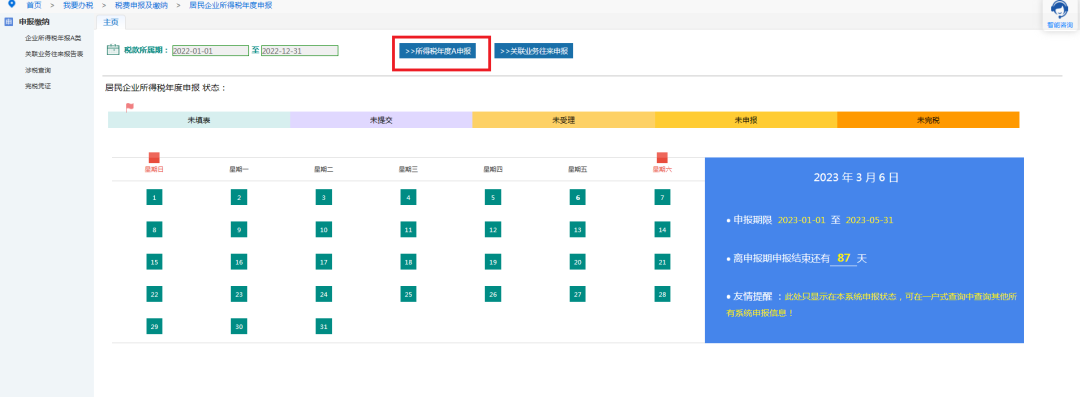

Please make the 2023 annual enterprise income tax return before May 31, 2024, and settle the enterprise income tax payable and refunded。

(2) the remittance time of the enterprise for cancellation of registration

Where a taxpayer needs to carry out enterprise income tax liquidation due to the termination of production and business, such as dissolution, bankruptcy, cancellation, etc., it shall report to the competent tax authorities before the liquidation, and complete the final settlement and payment of enterprise income tax to the competent tax authorities within 60 days from the date of the actual termination of business operations, so as to settle the tax payable and refunded。Where a taxpayer terminates its tax obligation according to law under other circumstances, it shall, within 60 days from the date of ceasing production or business operations, complete the final settlement and payment of the enterprise income tax to the competent tax authorities and settle the tax payable and refunded。

Select the applicable corporate income tax return

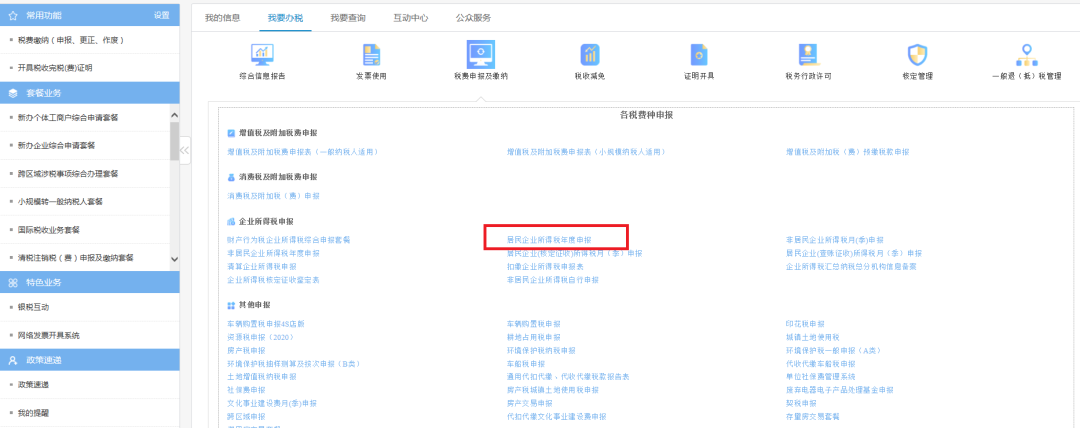

Annual Tax Return for Enterprise Income Tax of the People's Republic of China (Category A) and related schedules

The resident enterprises and the branches that implement the method of local pre-payment (consolidation) tax payment on a proportional basis

Annual Tax Return for Enterprise Income Tax of the People's Republic of China (Category B) and related schedules

Verify the expropriation of resident enterprises

Branch Enterprise Income Tax Annual Tax Return (Category A) and related schedules (table sample is the same as the People's Republic of China Enterprise Income Tax Monthly (Quarterly) Pre-Payment Tax Return (Category A))

A branch of a cross-regional business entity that collects tax payments

(2) Notes for report filling

Taxpayers who complete the Annual Tax Return of the People's Republic of China Enterprise Income Tax (Category A),Should first fill in the Enterprise Income Tax Annual Tax Return Form (hereinafter referred to as the "Form"),And according to the actual business of the enterprise in the year, select the corresponding schedule of "fill in" or "do not fill in" in the form,Where "complete" is selected,Regardless of whether the relevant business is subject to tax adjustment,The information in the attached table should be filled in completely。

小型微利企业可免于填报《最正规的买球APP下载》(A000000)中的 “主要股东及分红情况”、《最正规的买球APP下载》(A101010)、《正规堵球的APP》(A101020)、《正规堵球的APP》(A102010)、《正规堵球的APP》(A102020)、《正规堵球的APP》(A103000)、《最正规的买球APP下载》(A104000)。

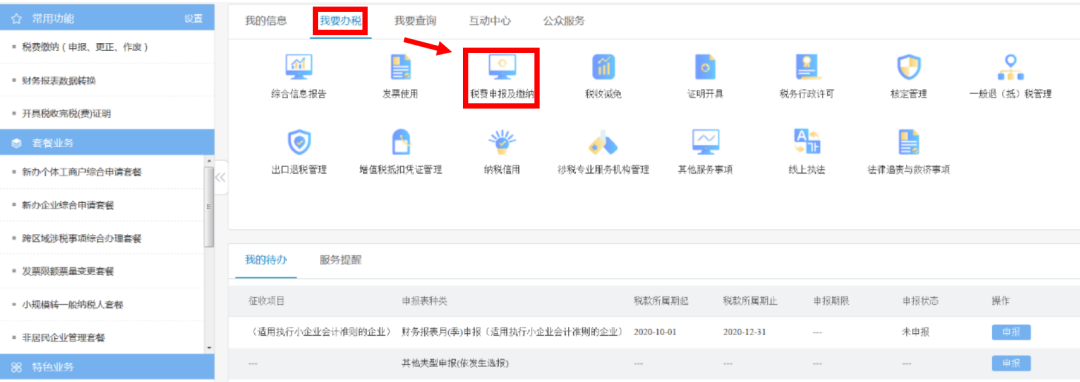

四、Final settlement declaration method

Enterprise income tax taxpayers can make remittance declaration through the electronic tax bureau, online declaration is more convenient, it is recommended that taxpayers choose online declaration。When the taxpayer cannot make online declaration, he can bring the relevant information of final settlement to the tax service hall。

Final settlement declaration process

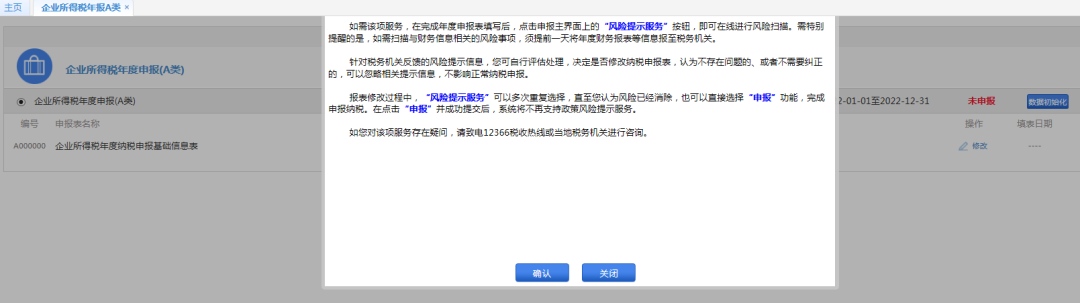

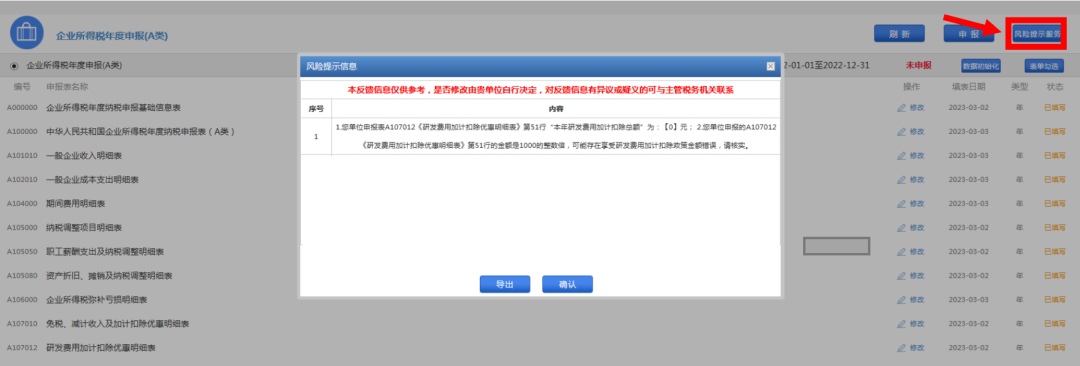

To help taxpayers prevent errors in the declaration process,Tax authorities rely on information technology and big data analysis methods,In the enterprise income tax annual online tax declaration link to provide taxpayers with annual declaration data pre-filling service and enterprise income tax policy risk warning service,To reduce taxpayer misstatement, misstatement,Defuse tax-related risks in advance。Taxpayers using the relevant service functions need to submit financial statements through online declaration one day in advance。

When taxpayers declare, the system will automatically obtain the income statement "operating income", "operating cost", "total profit" and other items according to the taxpayer's financial statement, and pre-fill the corresponding line of the enterprise income tax annual declaration form. Taxpayers can modify the pre-filled data。

When making the declaration, taxpayers can choose to click the "Risk Reminder Service", independently initiate the tax policy compliance risk scan, and modify the contents of the statement according to the scan results。When the taxpayer clicks "Submit declaration" after completing the declaration form and modifying the data correctly,The system will prompt "To improve the quality of your declaration data,Tax authorities have provided you with a tax compliance risk alert service",Taxpayers can click on "Risk Alert Service" for risk scanning,Based on risk scans,Click "Modify Form" to modify the report;You can also click "Submit Declaration",Skip the risk alert service,Continue to declare。

Before the 2023 final settlement of enterprise income tax declaration deadline (May 31, 2024), if the taxpayer finds that the annual declaration of enterprise income tax is wrong, it can correct it according to the circumstances。After the end of the final settlement period, if the taxpayer finds that there is an error in the annual return, he can make a correction through the electronic tax bureau。If more than one correction is required,Relevant supporting information should be provided,After examination by the competent tax authorities,Correct the declaration at the tax service hall;Or through the two sides of the tax agreement,After making an appointment at the electronic Tax office,The competent tax authorities shall open the function of electronic tax bureau to correct the declaration,Correct the declaration within the agreed time。If the correction of the declaration involves the payment of back taxes, a late fee will be charged on a daily basis from June 1, 2024。

The taxpayer shall truthfully fill out the annual tax return of the enterprise income tax, and submit the relevant information within the final settlement period, and bear legal responsibility for the authenticity and legality of the tax return and relevant information。

In order to further ease the financial pressure of taxpayers and reduce the tax burden, taxpayers should apply for tax refund in a timely manner when the annual tax declaration of enterprise income tax results in the final settlement of the overpaid tax, and the competent tax authorities will handle the tax refund in accordance with the relevant provisions。If the enterprise income tax paid in advance during the tax year is less than the enterprise income tax payable, the taxpayer shall promptly settle the enterprise income tax payable within the final settlement period。

For high-tech enterprises, technologically advanced service enterprises, animation enterprises, software integrated circuit enterprises that implement list management, non-profit organizations, cultural transformation enterprises, etc., taxpayers who need to obtain the corresponding qualifications can enjoy tax incentives according to regulations after obtaining the corresponding qualifications。

In order to help taxpayers get familiar with the policies and make accurate declarations, the tax bureau will carry out accurate policy publicity and guidance through portal websites, wechat public accounts, taxpayer schools and other means in combination with the needs of taxpayers。

Taxpayers can follow the portal website of Tianjin Taxation Bureau and the official wechat account of "Tianjin Taxation" to obtain information about corporate income tax policies,If the enterprise income tax returns encountered policy problems,This can be done by calling the telephone number published by the competent tax authority (available through the competent tax authority portal),Or through the 12366 service hotline, Tianjin Tax 12366 intelligent consulting service platform and "Tianjin Tax Pass" interactive cloud service to communicate and solve。

2023 annual corporate income tax settlement and settlement overview

Tax incentives for small and micro businesses

For small micro profit business yearTaxable income amountThe part not exceeding 3 million yuan shall be included in the taxable income amount at a reduced rate of 25%, and the enterprise income tax shall be paid at a tax rate of 20%。

From January 1, 2023 to December 31, 2027。

1.Announcement on Further Implementation of Preferential Income Tax Policies for Small and Micro Enterprises (Announcement No. 13, 2022, General Administration of Taxation of the Ministry of Finance)

2.Announcement on Preferential Income Tax Policies for Small and Micro Enterprises and Individual Industrial and Commercial Households (Announcement No. 6 of 2023 by the General Administration of Taxation of the Ministry of Finance)

3.Announcement on Further Supporting the Development of Small and Micro Enterprises and Individual Industrial and Commercial Households (Announcement No. 12 of 2023, General Administration of Taxation of the Ministry of Finance)

Research and development expenses are deducted

Research and development expenses actually incurred in R&D activities carried out by enterprises,Non-formed intangible assets are included in current profit or loss,On the basis of actual deductions in accordance with regulations,As of January 1, 2023,Then deduct 100% of the actual amount before tax;Forms intangible assets,As of January 1, 2023,200% of the cost of intangible assets is amortized before tax。

1.Announcement on Further Improving the Policy of Pre-tax Deduction of R&D Expenses (Announcement No. 7, 2023, General Administration of Taxation of the Ministry of Finance)

2.Announcement of the Ministry of Finance of the State Administration of Taxation on Matters related to Optimizing the Policy of Pre-payment Declaration enjoying Additional Deduction of R&D expenses (Announcement No. 11, 2023 of the Ministry of Finance of the State Administration of Taxation)

Enterprises recruit retired soldiers for independent employment

From January 1, 2023 to December 31, 2027,Enterprises recruit retired soldiers for independent employment,Sign a labor contract with a term of more than one year and pay social insurance premiums according to law,From the month when the labor contract is signed and social insurance is paid,Within 3 years, according to the actual number of recruits, VAT, urban maintenance and construction tax, education surcharge, and local education surcharge shall be deducted in turnCorporate income tax incentives。

The quota standard is 6,000 yuan per person per year, and the maximum can be raised by 50%. The people's government of each province, autonomous region and municipality directly under the Central Government may determine the specific quota standard within this range according to the actual situation of the region。

Announcement on Tax Policies for Further Supporting Self-employed ex-Soldiers to Start Businesses and Employment (Announcement No. 14, 2023, General Administration of Taxation, Ministry of Finance)

Enterprises recruit key groups

From January 1, 2023 to December 31, 2027,Companies recruit people out of poverty,And in the human resources and social security department of public employment service agencies registered unemployment for more than half a year and holding the "employment and entrepreneurship certificate" or "employment and unemployment registration certificate" (marked "enterprise absorption tax policy"),Sign a labor contract with a term of more than one year and pay social insurance premiums according to law,From the month when the labor contract is signed and social insurance is paid,Within 3 years, according to the actual number of employees, VAT, urban maintenance and construction tax, education surcharge, local education surcharge and enterprise income tax concessions will be deducted in turn。

The quota standard is 6,000 yuan per person per year, up to 30%, and the people's government of each province, autonomous region and municipality directly under the Central Government may determine the specific quota standard within this range according to the actual situation of the region。

The tax calculation basis of urban maintenance and construction tax, education fee surcharge and local education surcharge is the VAT tax payable before enjoying this preferential tax policy。

Announcement on Tax Policies for Further Supporting Entrepreneurship and Employment of Key Groups (Announcement No. 15, 2023, Ministry of Agriculture and Rural Affairs, Ministry of Human Resources and Social Security, General Administration of Taxation, Ministry of Finance)

Improve integrated circuit andIndustrial machineEnterprise R & D expenses shall be deducted

Integrated circuit enterpriseResearch and development expenses actually incurred during research and development activities with industrial mother-machine enterprises,Non-formed intangible assets are included in current profit or loss,On the basis of actual deductions in accordance with regulations,Between January 1, 2023 and December 31, 2027,Then deduct 120% of the actual amount before tax;Forms intangible assets,During the said period, 220% of the cost of intangible assets was amortized before tax。

1."Increase the proportion of additional deduction for R&D expenses of Integrated circuit and industrial mother-machine enterprises" (Announcement No. 44 of 2023 by the Ministry of Finance, General Administration of Taxation, National Development and Reform Commission, Ministry of Industry and Information Technology)

2.Notice on the Requirements for making a list of integrated circuit enterprises or projects and software enterprises that enjoy preferential tax policies in 2023 (Develope High-tech (2023) No. 287)

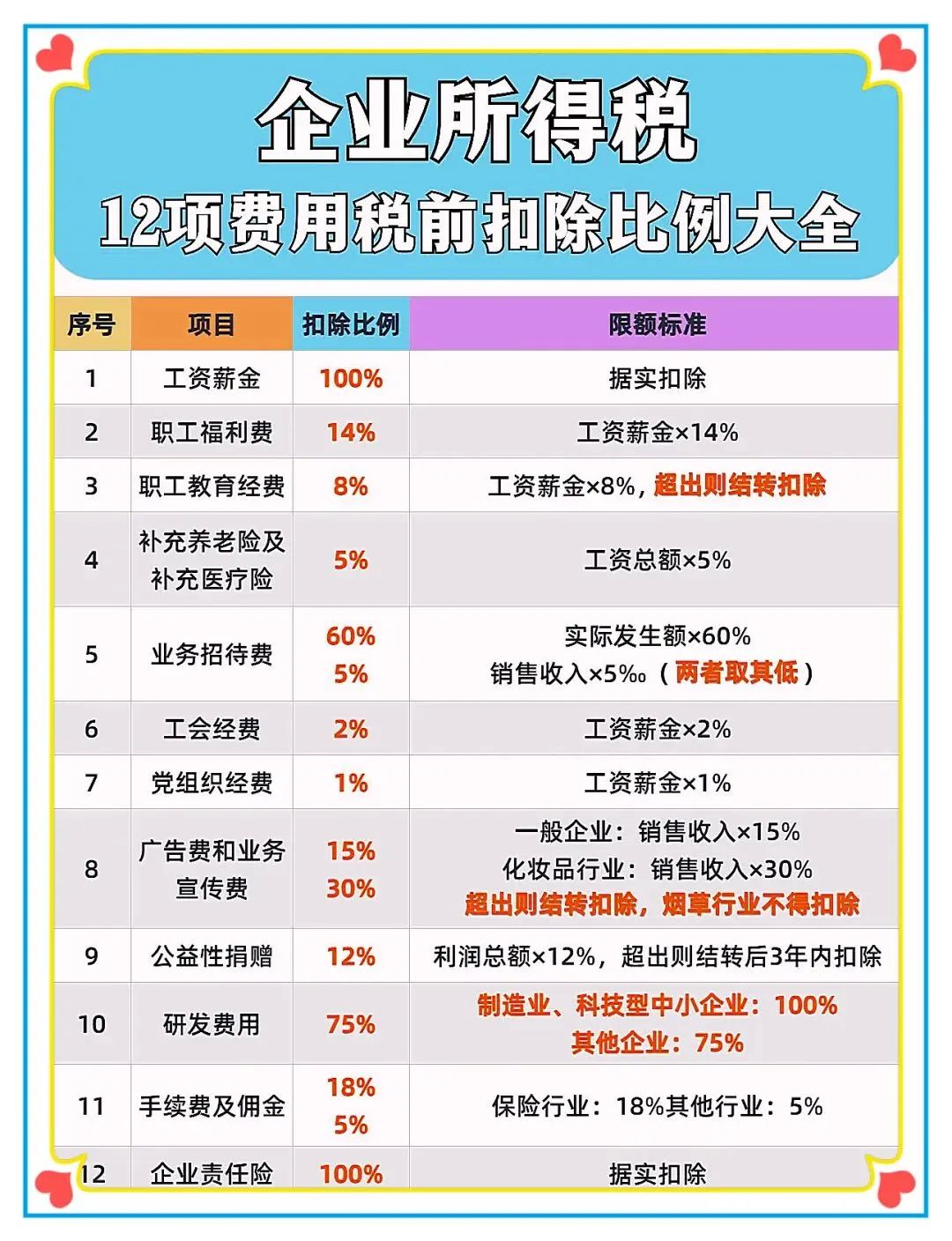

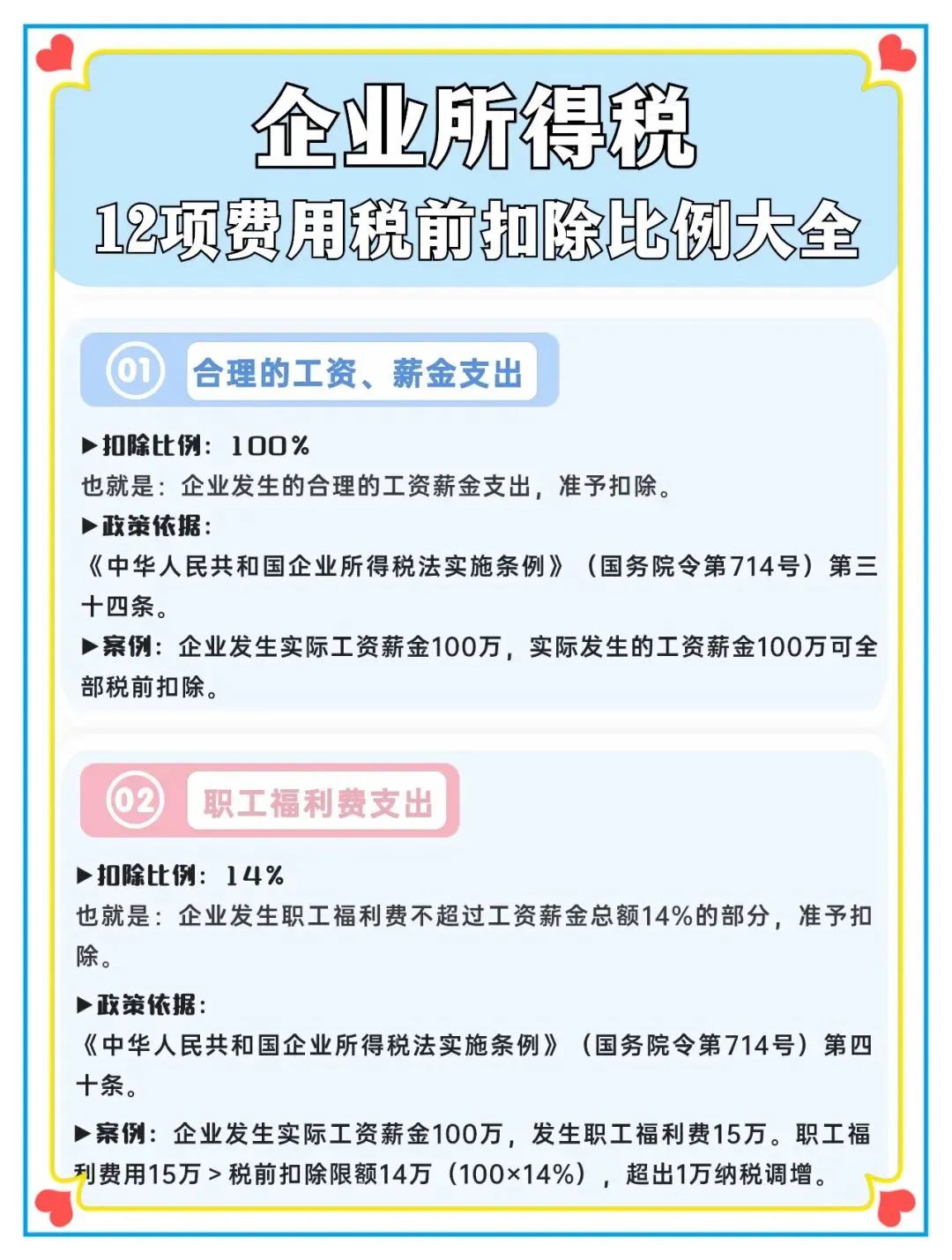

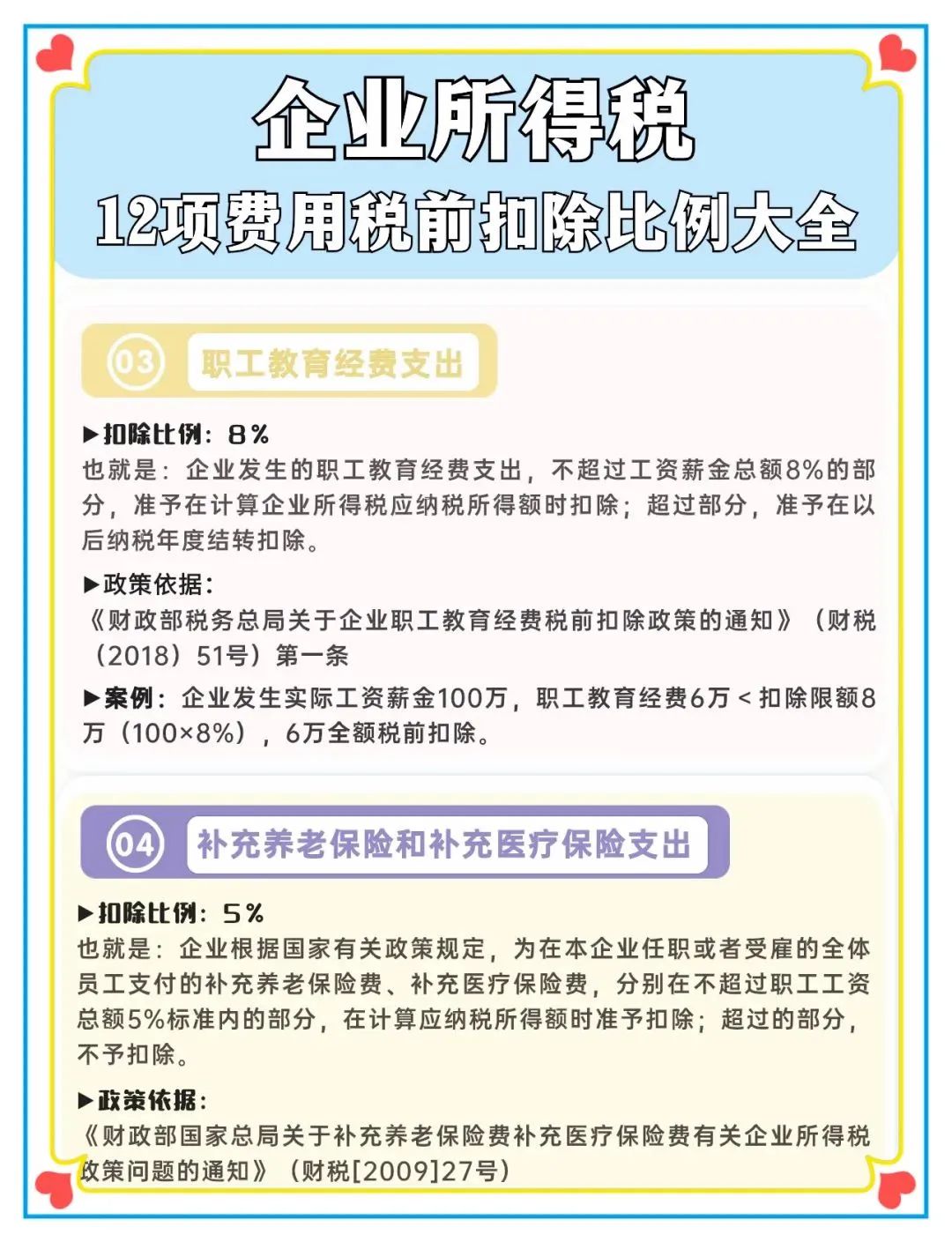

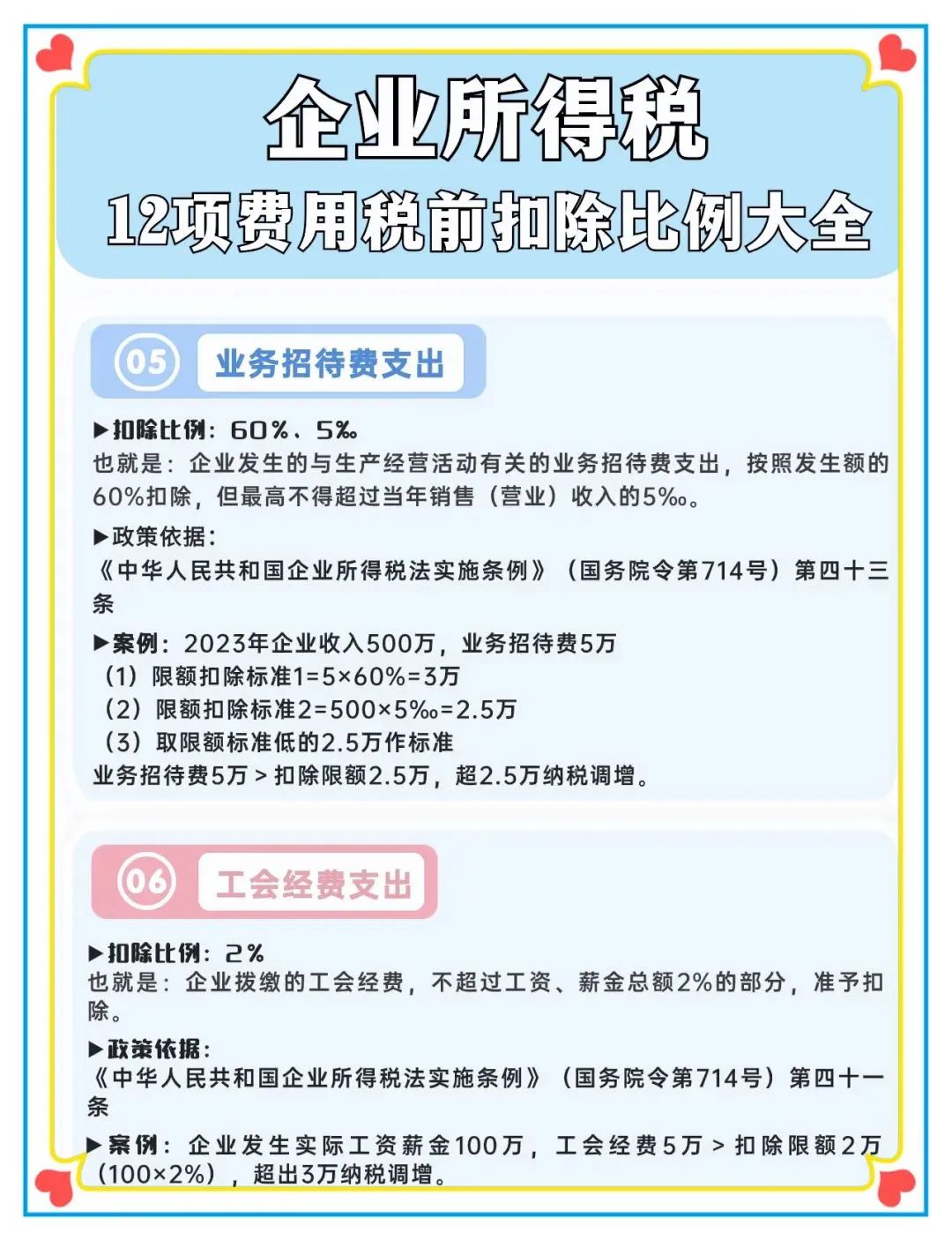

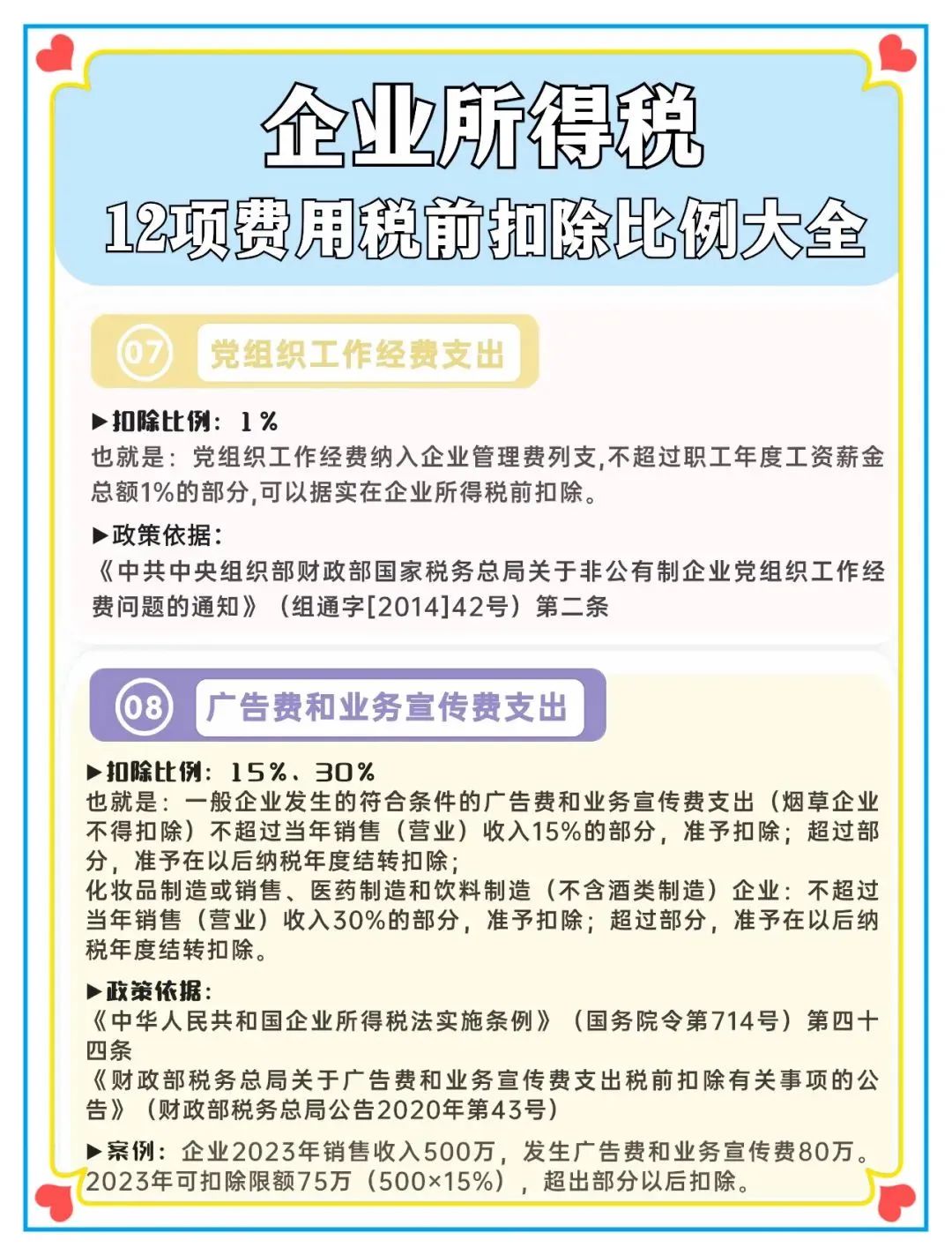

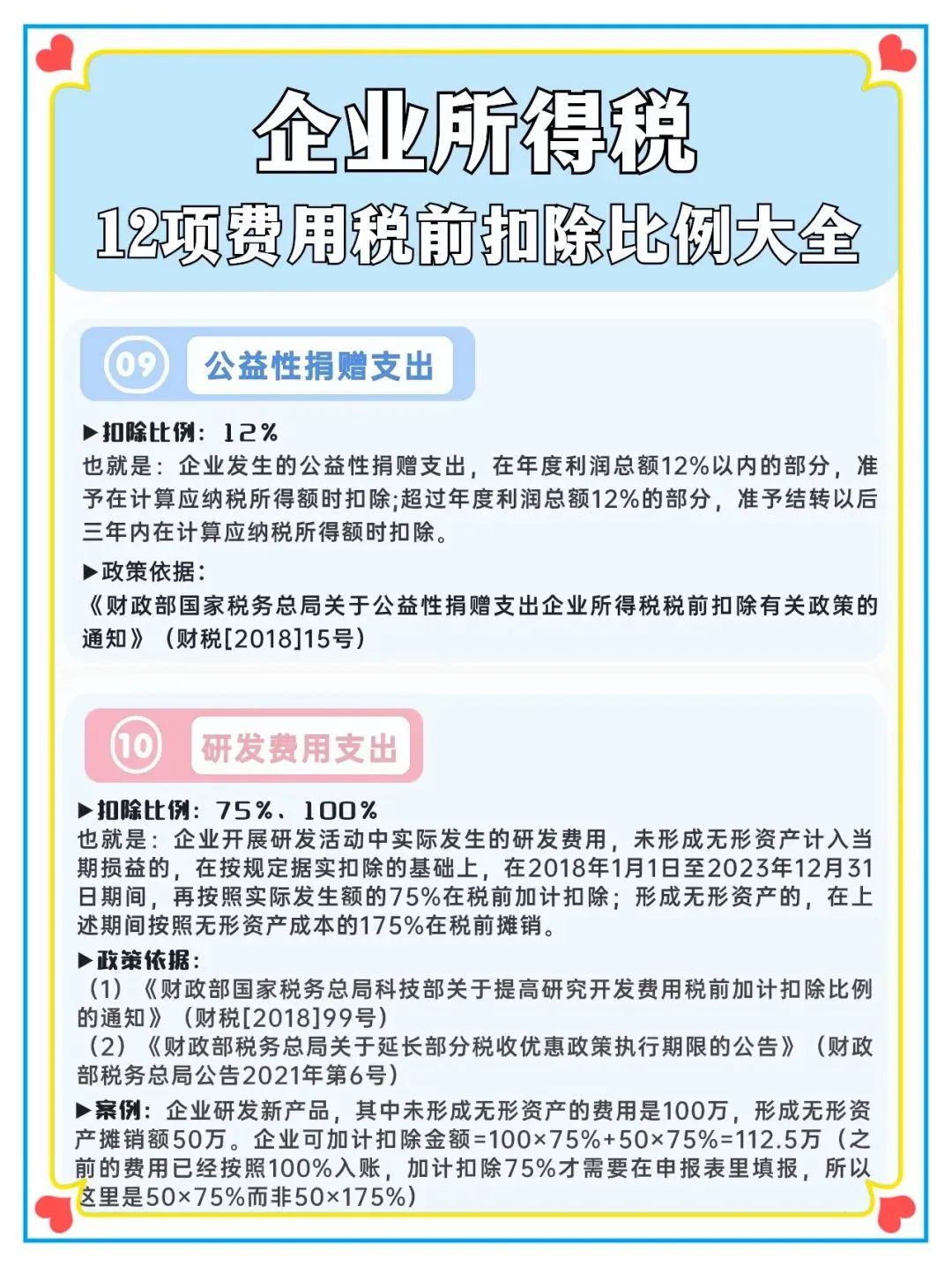

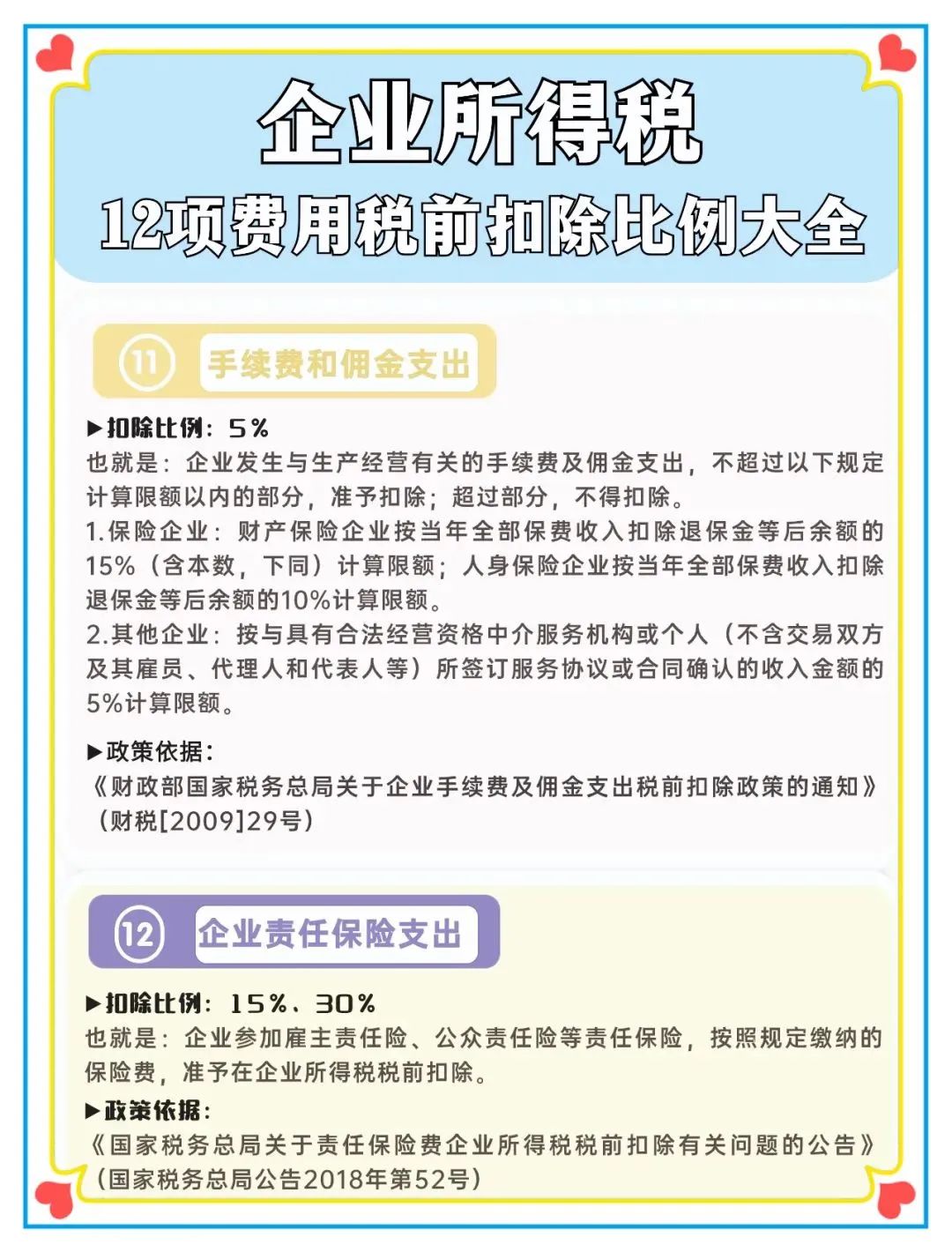

Corporate income tax 12 items of pre-tax deduction proportion of the total

1.In the year when the qualification of a high-tech enterprise expires, what tax rate shall be applied for the advance payment of the enterprise income tax before the re-identification?

A: According to the Announcement of the State Administration of Taxation on Issues related to the Implementation of Preferential Income Tax Policies for High-tech Enterprises (Announcement No. 24 of 2017 of the State Administration of Taxation) :The enterprise income tax shall be paid in the year after the expiration of its qualification as a new high-tech enterprise, before it is re-recognized暂按15%Where the tax rate is paid in advance and the qualification of a high-tech enterprise is not obtained before the end of the year, the corresponding period of tax shall be paid in arrearage according to the provisions。”

2.How is qualified non-profit organization income defined as tax-exempt income under the Corporate Income Tax Law?

A. According to Article 85 of the Regulations on the Implementation of the Enterprise Income Tax Law of the People's Republic of China (Order No. 512 of The State Council of the People's Republic of China), "The income of qualified non-profit organizations referred to in Article 26 (4) of the Enterprise Income Tax Law,It does not include income from non-profit organizations engaged in for-profit activitiesExcept as otherwise provided by the competent financial and tax departments under The State Council。”

According to the Notice of the State Administration of Taxation of the Ministry of Finance on the issue of Tax Exempt income of non-profit Organizations (Finance and Taxation [2009] No. 122), the following income of non-profit organizations is tax exempt income:

(1) Income from donations received from other units or individuals;

(2) Income from government subsidies other than fiscal appropriations provided for in Article 7 of the Enterprise Income Tax Law of the People's Republic of China, but excluding income derived from government purchase of services;

(3) membership fees collected in accordance with the regulations of civil affairs and financial departments at or above the provincial level;

(四)Untaxed incomeInterest income on bank deposits derived from tax-free income;

(5) other income prescribed by the Ministry of Finance and the State Administration of Taxation。”

3.What are the corporate income tax incentives for small, low-profit enterprises?

A: According to the Announcement of the State Administration of Taxation on Matters related to the Implementation of the Preferential income Tax Policy for the development of small micro-profit enterprises and individual industrial and commercial Households (Announcement No. 8 of 2021 of the State Administration of Taxation) : "(1) Matters related to the policy of halving the income tax of small micro-profit enterprises (1) The annual taxable income of small micro-profit enterprises does not exceed 1 million yuan,减按12.5%Included in taxable income,Pay corporate income tax at a rate of 20%。...Article 1 of this Announcement shall take effect as of January 1, 2021 and shall terminate on December 31, 2022。”

Second, according to the relevant provisions of the Announcement of the General Administration of Taxation of the Ministry of Finance on the Further Implementation of the Preferential Income Tax Policy for Small and micro Enterprises (Announcement No. 13 of the General Administration of Taxation of the Ministry of Finance 2022),From January 1, 2022 to December 31, 2024,For small micro profit business yearTaxable income amount超过100万元但The part not exceeding 3 million yuan shall be included in the taxable income amount at a reduced rate of 25%, and the enterprise income tax shall be paid at a tax rate of 20%。

(3) According to the relevant provisions of the "Announcement on Preferential Income Tax Policies for Small and Micro Enterprises and individual Industrial and Commercial Households" (Announcement No. 6 of 2023 by the General Administration of Taxation of the Ministry of Finance),From January 1, 2023 to December 31, 2024,The part of the annual taxable income of small low-profit enterprises not exceeding 1 million yuan,Deduct 25% from taxable income,Pay corporate income tax at a rate of 20%。

4.The enterprise meets the conditions of the two preferential policies of R&D expense deduction and small micro-profit enterprise at the same time, whether the two preferential policies can be enjoyed at the same time?

A: According to Article 2 of the Notice of the State Administration of Taxation of the Ministry of Finance on Several Issues concerning the Implementation of the Preferential Policy of Enterprise Income Tax (Finance and Taxation [2009] 69),Notice of The State Council on the Implementation of Transitional Preferential Policies for Enterprise Income Tax (Guofa [2007] No. 39) Article 3 shall not be superimposed,And once selected,No change in tax preference,Limited to the transitional preferential policy of enterprise income tax and the regular tax exemption and tax rate reduction provided for in the Enterprise Income Tax Law and its implementing regulations。The various tax preferences provided for in the Enterprise Income Tax Law and its implementing regulations,Any enterprise that meets the prescribed conditions can enjoy it at the same time。

Therefore, if the enterprise meets the conditions of research and development fee deduction and small small profit enterprise preference, it can enjoy it at the same time according to the regulations。

5.The new policy of deduction of R&D expenses for small and medium-sized enterprises in science and technology will be implemented from January 1, 2022. When our company goes through the 2022 annual final settlement, what kind of warehouse registration number is needed to enjoy the policy of deduction of R&D expenses in 100% proportion?

A: According to the "Notice of the State Administration of Taxation of the Ministry of Science and Technology on Matters related to the evaluation of Science and Technology smes" (National Science and Technology Fire [2018] No. 11), the provincial science and technology management departments should followThe date of establishment of the enterprise and the date of submitting the self-assessment information shall be marked on the registration number of the technology-based smes。

The specific coding rules are: established before the year of storage and submit self-assessment information before May 31,The 11th digit of its registration number is 0;Established before the warehousing year but submitted self-assessment information after June 1 (inclusive),The 11th digit of its registration number is A;Established in the year of storage,The 11th digit of its registration number is B。Among them, the 11th place of the warehouse registration number is 0, which can enjoy the research and development expenses of small and medium-sized enterprises in the last year's final settlement and deduction policy。

According to the above provisions, if your company has R & D expenses in 2022, if you enjoy the deduction of 100% of the R & D expenses of science and technology smes at the time of the 2022 annual settlement, you need to obtain the warehousing registration number of the 11th 0 science and technology smes in 2023。

It is considered that there is a time requirement for enterprises to obtain the warehousing registration number with the 11th digit being 0,It is recommended that your company comply with the provisions of the "Evaluation Measures for Small and medium-sized Enterprises in Science and Technology" (issued by Guoke Anger (2018) No. 11),If possible, obtain the 2023 warehouse registration number before the end of the final settlement,Ensure timely and accurate access to offers。

6.Can the wages and salaries withheld by an enterprise in December of the current year and paid in January of the following year be deducted when the enterprise income tax is settled in the current year?

A: According to Article 2 of the Announcement of the State Administration of Taxation on the issue of Pre-tax deduction of Enterprise Wages and Salaries and employee welfare expenses (the State Administration of Taxation Announcement No. 34 of 2015), enterprisesThe wages and salaries actually paid to employees before the end of the annual settlement are allowed to be deducted in accordance with the provisions of the annual settlement。As stipulated in Article 4, this announcement applies to the final settlement and payment of enterprise income tax for the year 2014 and subsequent years。Matters that have not been processed for tax purposes before the implementation of this announcement may be implemented in accordance with this Announcement if they comply with the provisions of this Announcement。

Therefore, the wages and salaries withheld by the enterprise in December of the year, which are paid in January of the following year, can be deducted in accordance with the regulations when the final settlement of the enterprise income tax in the current year。

7.What are the preferential policies of enterprise income tax for the placement of disabled persons in employment?

A: In accordance with the relevant provisions of Article 30 of the Enterprise Income Tax Law of the People's Republic of China (Order No. 63 of the President of the People's Republic of China), the wages paid for the placement of disabled persons and other employment personnel encouraged by the State may beAdd deductions to the calculation of taxable income。

According to the provisions of Article 96 of the Regulations on the Implementation of the Enterprise Income Tax Law of the People's Republic of China (Order No. 512 of The State Council of the People's Republic of China),An additional deduction shall be made for the wages paid by an enterprise for the placement of disabled persons as mentioned in item (2) of Article 30 of the Enterprise Income Tax Law,It refers to the placement of disabled persons by enterprises,On the basis of actual deductions from the wages paid to disabled employees,The deduction is based on 100% of the wages paid to disabled employees。The scope of disabled persons shall be governed by the relevant provisions of the Law of the People's Republic of China on the Protection of Disabled Persons。

Third, according to the provisions of Article 1 of the Notice of the State Administration of Taxation of the Ministry of Finance on the Preferential Policy of Enterprise Income Tax on the placement of disabled persons in Employment (Finance and Taxation [2009] No. 70),The enterprise places disabled persons,On the basis of actual deductions from the wages paid to disabled employees,The taxable income can be deducted according to 100% of the salary paid to the disabled employee。

An enterprise shall allow the deduction of wages paid to employees with disabilities to be calculated according to the actual facts when making the enterprise income tax advance declaration;At the end of the year, when the annual declaration and final settlement of the enterprise income tax are made, the additional calculation and deduction shall be made in accordance with the provisions of the first paragraph of this article。

8.If the relevant costs and expenses actually incurred by the enterprise in the current year cannot be obtained in time due to various reasons, how should the enterprise income tax be handled in the quarterly advance payment and final settlement?

Answer: According to the provisions of Article 6 of the "Announcement of the State Administration of Taxation on several Issues of Enterprise Income Tax" (the State Administration of Taxation Announcement No. 34, 2011), the relevant costs and expenses actually incurred by the enterprise in the current year, due to various reasons, the effective vouchers of the costs and expenses are not obtained in timeWhen the quarterly income tax is paid in advance, it can be temporarily calculated according to the book amount;但At the time of final settlement and settlement, the valid proof of such cost and expense shall be provided。

Article 7 This announcement shall take effect as of July 1, 2011。Before this announcement goes into effect,The relevant matters occurring in the enterprise have been handled in accordance with the provisions of this announcement,No longer adjust;Have dealt with,However, the treatment is inconsistent with the provisions of this announcement,Where it is necessary to adjust or reduce the taxable income amount in accordance with the provisions of this announcement,The taxable income of the enterprise in 2011 shall be reduced accordingly after the implementation of this announcement。

9.Can the late payment of the social security fee paid by the unit be deducted before tax when the income tax is settled?

A: According to Article 10 of the Enterprise Income Tax Law of the People's Republic of China, "When calculating the taxable income amount, the following expenditures shall not be deducted:

(1) dividends, bonuses and other equity investment proceeds paid to investors;

(2) enterprise income tax;

(3) tax late fees;

(4) fines, fines and losses of confiscated property;

(5) Donations other than those provided for in Article 9 of this Law;

(6) sponsorship expenditure;

(7) unapproved reserve expenditures;

(8) Other expenditures unrelated to the acquisition of income。”

因此,Late payment of social security fees can be paid before the enterprise income tax。

10.How to determine the caliber of "total income" and "high-tech products (services) income" when a high-tech enterprise is identified?

A: According to the relevant provisions of the Notice of the State Administration of Taxation of the Ministry of Science and Technology and the Ministry of Finance on the Revision and Issuance of the Guidelines on the Identification and Administration of High-tech Enterprises (Guofa Fire (2016) No. 195) document,Gross income is total income less untaxed income。Sales income is the sum of main business income and other business income。

High-tech products (services) revenue refers to the enterprise through research and development and related technological innovation activities,The sum of product (service) revenue and technology revenue obtained。

Annual enterprise income tax final settlement online declaration operation guide

There are some differences in the operation of electronic tax bureaus around the country, mainly master the principle, taking Jiangsu Province as an example。

1. Log in to the electronic tax Bureau

Taxpayers please log in through Jiangsu Electronic Tax Bureau of State Administration of Taxation。

(http://etax).jiangsu.chinatax.gov.cn/ )

Select "Tax Declaration and Payment" in the "I Want to do Tax" module。

Click the "Annual Declaration of Resident enterprise Income Tax" module。

Enter the declaration module, the system displays the tax declaration period, declaration status, declaration deadline and other information。Click "Income Tax Annual A Declaration" (applicable to audit and collection enterprises) or "Entry declaration" (applicable to approved collection enterprises), and the system will display the annual return of enterprise income tax。

1.The Electronic tax Bureau has opened the "risk warning service" function. After completing the annual declaration form, the risk scan can be carried out online. If the risk matters related to financial information need to be scanned, the annual financial statement and other information must be reported to the tax authorities one day in advance。

2.The electronic tax Bureau reminds taxpayers that after the completion of the declaration, if there is an overpayment of the final settlement, they can immediately submit a tax rebate application through the electronic tax Bureau。

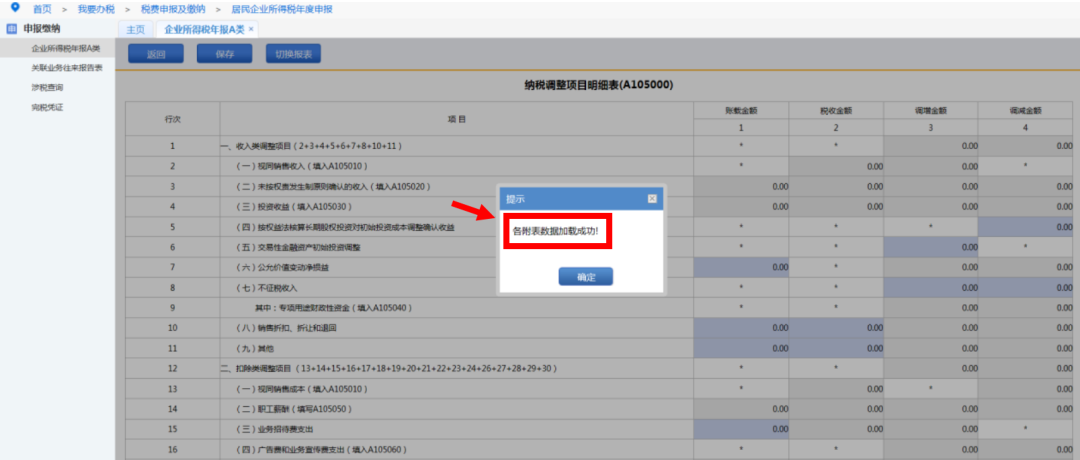

Click "Data initialization", the system automatically obtains the tax registration information of the relevant report, the number of carry-over of the relevant form in the last year and other data. The system displays "initialization succeeded", and click "OK" to complete the data initialization。

Note: If the system does not display reportable statements or display reportable statements incomplete, please contact the tax authorities。If the report has been filled in, use this function with caution. Otherwise, the data in the report will be cleared。

Click "Modify" to enter the application form filling page。

The order of filling in the form is divided into the following three situations:

① Approved collection enterprises directly fill in the Annual tax return of Resident Enterprise Income Tax (applicable to approved collection), and can optionally report the Information Report Form of Resident Enterprises' participation in foreign Enterprises.。

② The branch can fill in the Annual Tax Return of the branch of the cross-regional business summary tax payment Enterprise and return to the list page after saving。

③ Non-small micro-profit enterprises collected by audit:

Step 1:Fill in the "A000000 Enterprise Income Tax Annual Tax Return Basic Information Form", the electronic tax bureau generates most of the data for the taxpayer based on the tax registration, pre-payment declaration and other information, please check and modify the taxpayer to save the form。

Step 2:Fill in "Enterprise Income Tax Annual Declaration Form A",There are two ways to fill out the form,First, the system automatically jumps out of the "Form" for taxpayers to fill in after the "A000000 Annual Enterprise Income Tax Return Basic Information Form" is saved;Second, taxpayers can click the "form check" button in the upper right corner of the list page to fill in。

Note:Later, when the "A000000 Annual Basic Information Form of Enterprise Income Tax Return" is modified and saved, the "Form" will be given for selection. Users can select the form again according to the actual situation, and the data filled in the original selected form will be retained。When the form is checked and clicked, the system will prompt the report to be checked according to the filling situation of the user's basic information form, and the user can judge according to their actual situation. If the corresponding form needs to be added, click cancel and then check the corresponding form to determine。

Step 3: After filling in form A101010 to Form A104000, return to the main form A100000, click "Read data", fill in other data that can be filled in, check and save。

Note:If the report number is smaller than A104000, fill in the selected report first; otherwise, the accurate filling in of subsequent reports will be affected.To obtain the associated table data, please click the "data read" button in the form filling page, and there is a "Report switch" button in the form filling page for switching forms。

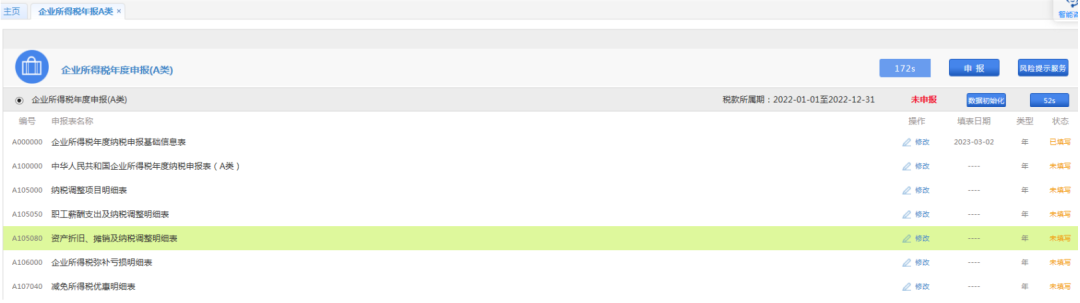

Step 4:First fill in the attached schedule of the A105000 form (such as: A105050 form, A105080 form, etc.), then fill in the A105000 form, and then open the A100000 form "read data" check and save。

【正规堵球的APP】

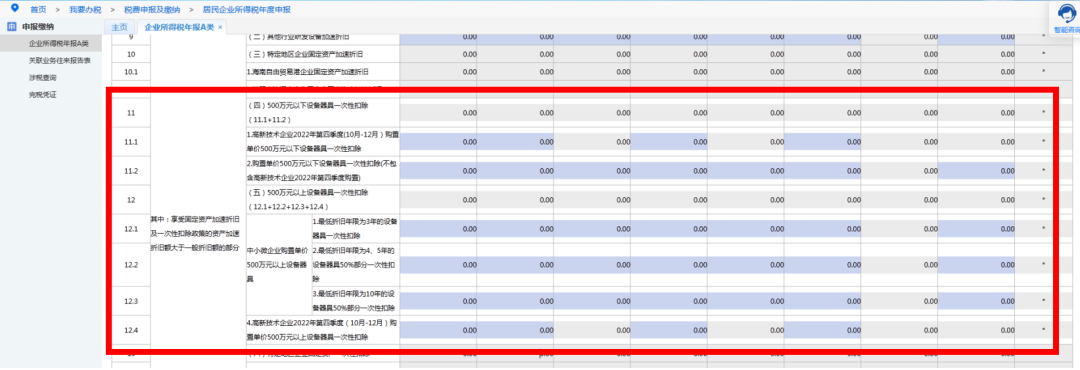

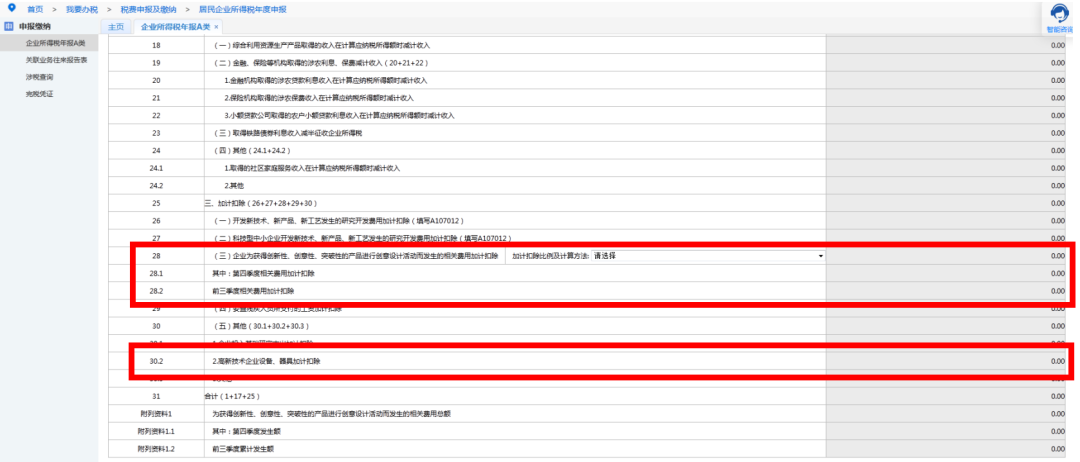

1.In 2022, the A105080 table was newly revised, and the new preferential policies such as "one-time deduction of equipment purchased by high-tech enterprises in the fourth quarter of 2022 (October to December)" and "proportional deduction of equipment purchased by small, medium-sized and micro enterprises with a unit price of more than 5 million yuan" were added。

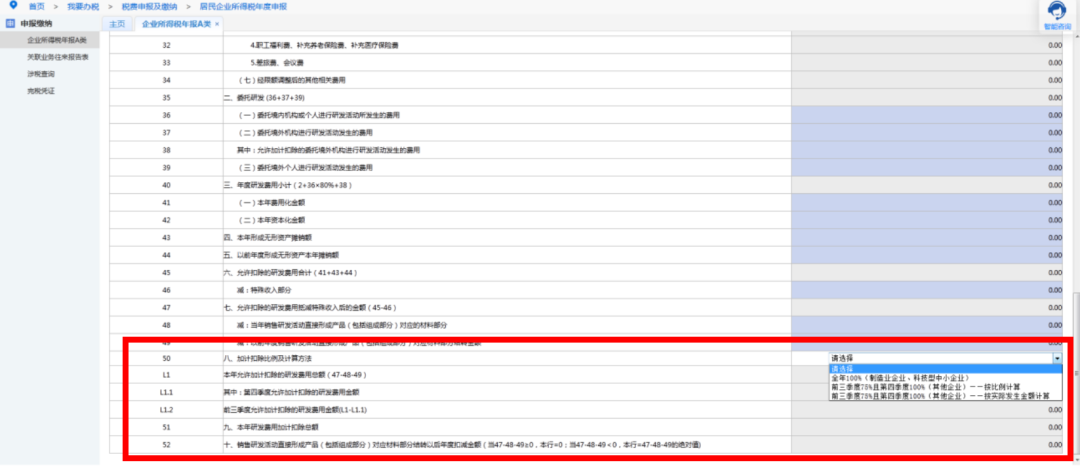

2.In 2022, the newly revised A107012 form, manufacturing enterprises and scientific and technological smes are deducted by 100% extra for the whole year;For other enterprises, 75% shall be deducted in the first three quarters, and 100% shall be deducted in the fourth quarter. The calculation method can be calculated according to the proportion or according to the actual amount。

3.In 2022, the A107010 table was newly revised, and the entry column of the new preferential policy of "high-tech enterprise equipment and equipment additional deduction" was added。

If the enterprise enjoys "additional deduction of expenses related to creative design activities for obtaining innovative, creative and breakthrough products",Manufacturing enterprises and small and medium-sized scientific and technological enterprises shall be deducted by 100% extra for the whole year;Other enterprises in the first three quarters by 75%,In the fourth quarter, it was deducted at 100% plus,The calculation method can be selected on a proportional basis or according to the actual amount。

Step 5:Fill in A106000, open table A100000 "Read Data", check and save。

④ small micro-profit enterprises collected by audit:

Step 1:Fill in the "A000000 Enterprise Basic Information Form", the electronic tax bureau generates most of the data for the taxpayer based on the tax registration, pre-payment declaration and other information, please check and modify the taxpayer to save the form

Note:The relevant data in this table are related to the enjoyment of income tax incentives for small and micro enterprises and the push judgment of the income and expenditure schedule. Please fill it in carefully;Please contact the competent tax authority if you find incorrect data that cannot be modified。

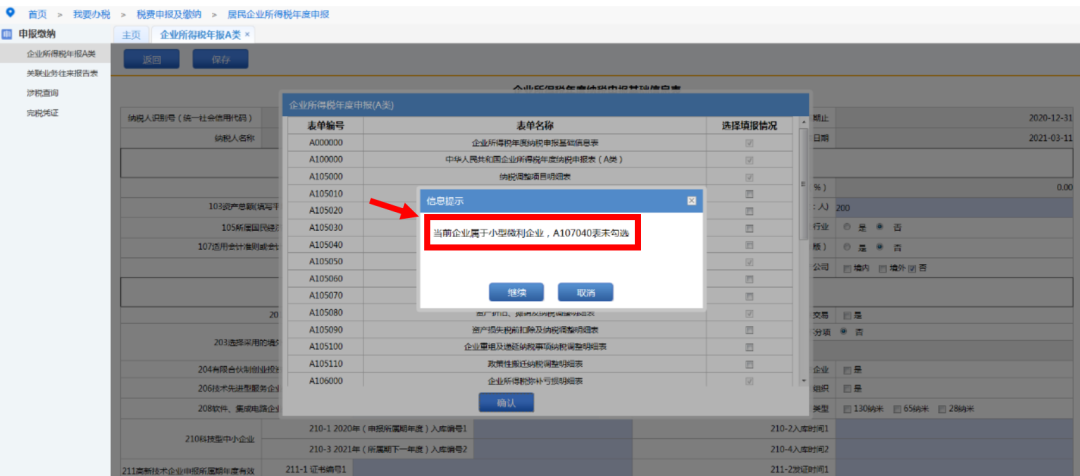

Step 2:Fill in the "Enterprise Income Tax Annual Declaration Form A", if you meet the conditions of small micro-profit enterprises, the system will prompt you to check the A107040 form。Other operations are consistent with non-small, low-profit enterprises。

No need to fill out form A101010 to Form A104000 for small micro-profit enterprises。

Step 3:If you have already declared the financial statements, you can directly import the operating income, operating cost and other data on the financial statements through the "Import Financial Statements" function。

Step 4:Fill in the attached schedule of form A105000, and fill in the same as non-small micro-profit enterprises。

Step 5:Fill in A106000, open table A100000 "Read Data", check and save。

Step 6:Fill in form A107040 (small and micro reduction), then open form A100000 "Read data" check and save。Otherwise, the declaration will prompt abnormal small and micro preferential information。

Note:The taxpayer can fill in the report according to the actual situation. If the selected report has no value, it needs to open the report and save the empty table。

After all the reports are filled in and the data is verified correctly, click the "declaration" button. If there is any error, the system will give an error message, and the user (taxpayer) can modify and declare again according to the prompt or verification information。

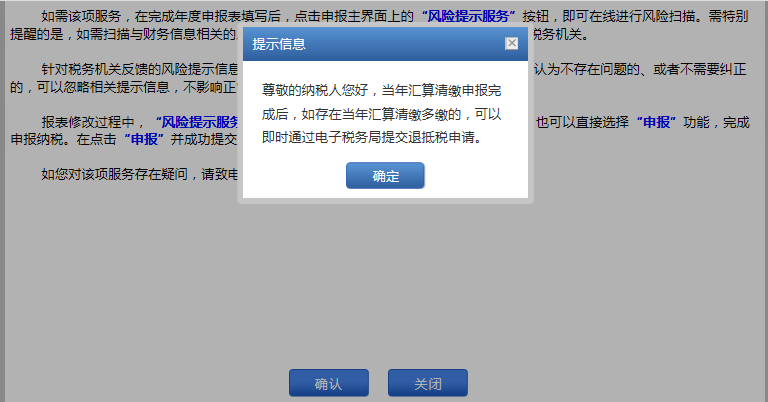

Before submitting the declaration, you can choose the "risk warning service" to conduct risk scanning online, evaluate and deal with the risk warning information according to the feedback, and decide whether to modify the declaration form. If you think that there is no problem or need to correct, you can ignore the relevant warning information and do not affect the normal tax declaration。

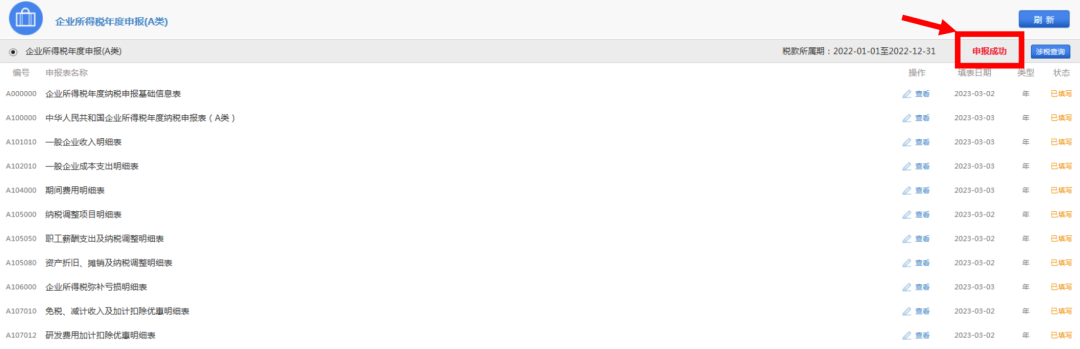

If there is no error information or verification feedback, wait for a moment to refresh the page, and the system displays "declaration success" to complete the declaration。

[Tips] After the completion of the declaration, if there is an overpayment of the final settlement, you can immediately submit a tax refund application through the electronic tax bureau。

4. The declaration is invalid

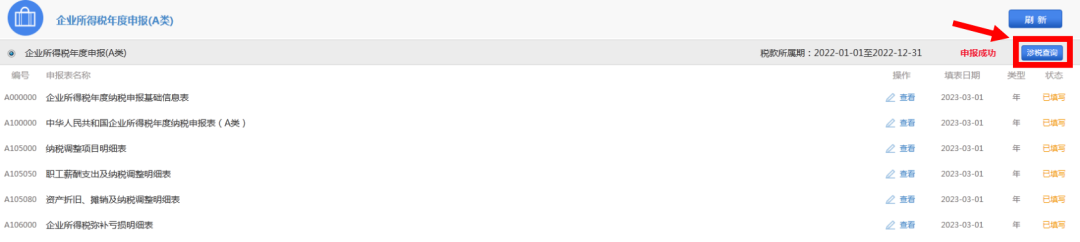

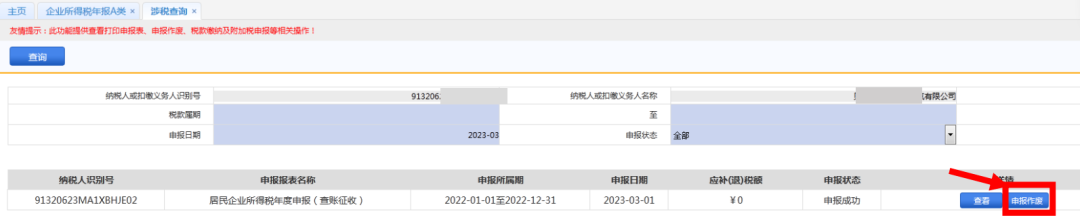

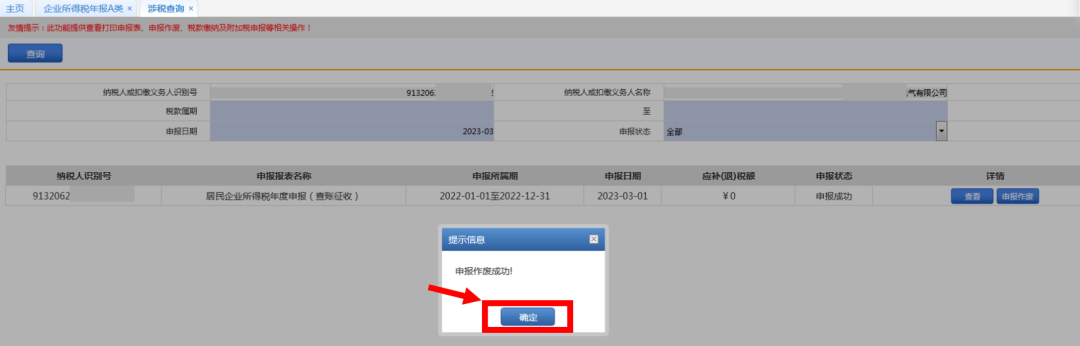

If the payment letter is not issued after the successful declaration, the taxpayer finds that the declaration is wrong, it can click the "tax-related inquiry" button on the right side of "declaration success" or click the "tax-related inquiry" on the left side of the page to view the corresponding declaration by entering the period and other conditions, and click the "Declaration nullification" button to cancel the declaration。

Note: If the payment letter has been issued, you must go to the competent tax authority to cancel the payment letter and then cancel the declaration or come to the house to correct the declaration。

Click "Declaration inquiry", you can query, preview, download and print the declaration form。If you cannot preview and print, go to the Download Center to download and install the print controls and Adobe Reader。

结语:The final settlement is not only a tax obligation, but also the embodiment of the enterprise's internal control and financial management level。Enterprises should pay attention to this link as an important opportunity to improve their financial management level and tax compliance。In the process of final settlement, planning possible preferential tax policies, reasonable arrangement of pre-tax deduction items and other strategies are also important measures for enterprises to reduce costs and increase efficiency。By handling the final settlement and settlement well, enterprises can not only avoid unnecessary tax risks, but also optimize the allocation of financial resources and enhance the market competitiveness of enterprises on the basis of tax compliance。